Policy Brief

Social Security

Introduction

Jersey has a comprehensive social security system providing a wide range of benefits. This Brief provides key data about the system, drawing on the limited amount of easily accessible information. The statistics have been obtained from several different sources including the Government's annual Budgets and Annual Accounts, a response to a Freedom of Information request and the statistics on https://opendata.gov.je.

Summary

- Social Security systems are government-run programmes to provide financial protection and support to individuals and families.

- In practice, social security systems do not operate in isolation but rather are part of the wider public policy framework, including the income tax regime, other benefits and political priorities of the day.

- Jersey’s social security system is funded by contributions from employers and employees and tax revenue.

- Currently, employees earning above £553 a month pay a contribution of 6.0% up to an upper limit of £5,800. Employers pay a contribution of 6.5%, and 2.5% on earnings in excess of the upper limit. Self-employed people pay contributions equal to those that an employer and employee would pay.

- In 2024, £403 million was paid into the social security scheme. 40% comprised contributions by employers and 34% contributions by employees. The self-employed contributed 6%, of which 3.6% can be attributed to their capacity as employers and 2.4% to their capacity as employees. Tax revenue contributed the remaining 19%.

- Benefits totalling £387 million were paid in 2024, of which pension payments accounted for £255 million.

- The full state pension is £14,899 a year. Entitlement depends on the period for which contributions have been made, not the amount of contributions.

- The Health Insurance Fund paid benefits of £52 million in 2024, mainly to help meet the cost of GP appointments and drugs for low income people.

- The Social Security (Reserve) Fund, which largely exists to meet pension liabilities, stood at £2,452 million at end-2024.

- The Long Term Care Fund is funded separately by an additional 1.5% levy on income tax. Revenue in 2024 was £45 million but payments were £80 million, necessitating a significant contribution from tax revenue.

- Income support is funded out of general taxation not social security contributions and is paid to those with incomes below specified thresholds. Income support also meets rental costs within certain limits. Income support payments totalled £78 million in 2024 of which £34 million was to meet housing costs.

- The Community Cost Bonus provides an annual payment of £516.50 to low income families who are not eligible for income support.

- A key long term policy issue is the implications of the ageing society.

- Jersey has largely managed to avoid key problems in the UK social security system, particularly the effect of the benefit system on willingness to work.

Social security systems – an overview

Social Security systems are government-run programmes designed to provide financial protection and support to individuals and families when certain life events disrupt or terminate their income, or when they incur exceptionally heavy expenses. While specific features vary by country, the basic components generally include -

- Funding Mechanism:

- Contributions: The most common funding method involves contributions from workers and employers, generally through payroll taxes.These contributions are typically placed into designated funds and are used to pay benefits to current recipients. This system often operates on a "pay-as-you-go" basis, meaning current contributions fund current benefits, rather than funding future benefits for current contributors.

- General Taxation:Some social security benefits, especially means-tested ones, may be funded through tax revenue.

- Eligibility Requirements:

- Work Credits/Contribution History:For many benefits, especially retirement, disability and survivor benefits, eligibility is tied to a person's work history and the contributions they have paid into the system over time.

- Age:Retirement benefits are generally available on reaching a certain age, with provisions for early or delayed retirement affecting the benefit amount.

- Specific Circumstances:Eligibility for other benefits (eg disability, unemployment) depends on meeting specific criteria related to the event (eg medical certification of disability, job loss due to no fault of their own).

- Means-Testing:Some benefits are "means-tested," meaning eligibility and/or benefit amount depend on the recipient's income and assets, targeting support to those with the greatest financial need.

- Types of Benefits:Social security systems typically provide a range of benefits -

- Pensions:monthly payments to people who have reached a specified age and have a sufficient contribution history.

- Disability Benefits:Financial support for workers who become unable to work due to a significant illness or injury, and who have contributed to the system.

- Survivor Benefits:Payments to eligible family members of a deceased worker who had paid into the system.

- Unemployment Benefits:Temporary income support for individuals who have lost their jobs through no fault of their own and are actively seeking employment.

- Sickness and Maternity/Parental Benefits:Payments during periods of illness, childbirth or for parental leave.

- Family Allowances/Child Benefits:Regular payments to families with children, to help with the costs of raising them.

- Healthcare Provision:In some systems, social security also encompasses or is closely linked to national health schemes, providing access to medical care.

- Other Specific Benefits:Depending on the country, there may be benefits for specific needs like industrial injuries, long-term care or funeral expenses.

- Benefit Calculation:

- Earnings-Related:Some benefits, particularly retirement and disability, are calculated based on a worker's lifetime earnings, aiming to replace a portion of their pre-event income. Higher earnings may lead to higher benefits.

- Cost-of-Living Adjustments:Benefits are often adjusted periodically to account for inflation, helping to maintain their purchasing power over time.

- Flat-Rate:Some benefits might be a fixed amount, regardless of prior earnings.

- Administration:

- Social security systems are typically administered by a government agency or a semi-public body responsible for collecting contributions, determining eligibility, calculating benefits and making payments.

In essence, a social security system aims to provide a safety net and a degree of income stability for individuals throughout various stages of their lives, protecting them from the financial impacts of common life risks.

Social security and wider policy issues

In practice, social security systems do not operate in isolation but rather are part of the wider public policy framework, particularly the income tax structure, other benefits and political priorities of the day.

In many systems the contributions are insufficient to meet the benefits so governments have to “top up” contributions.

Conversely, contributions may be seen as another form of tax, one easier to increase than direct taxes on incomes. In 2024, the UK Labour Government, having committed to not increasing taxes on “working people”, raised employer national insurance contributions, simply as a tax raising measure. Indeed, there are suggestions that tax and social security contributions should be merged, something which would weaken the principle of benefits being linked to contributions.

There are a number of issues relevant to all social security systems, which require political decisions to be taken –

- When new benefits are introduced, the contributions are unlikely to be able to fund the benefits. This applies particularly to pensions as by definition a period of many years must elapse before sufficient contributions have been made to provide a full pension.

- Whether benefits should be means tested. If they are not then they can be expensive, requiring higher contributions or taxes. Where they are then the system becomes complicated and there can be a high marginal tax/loss of benefit rate when someone moves from being eligible to not being eligible.

- The extent to which the system redistributes income from high paid to low paid people. In respect of pensions this is done by the pension being largely based on the number of years for which contributions have been paid, not the amount of the contributions.

- The effect on incentives to work. There is a risk that a generous benefit system can reduce incentives to work. In extreme cases, people can be better off financially though benefits than if they were in low paid work. In the UK recently there has been a huge increase in the number of people seeking disability benefit as this is financially more generous than unemployment benefit.

- The position of migrants. Should there be a minimum period before a migrant can claim benefits even though they are making contributions? Given extensive migration there are reciprocal arrangements between jurisdictions in respect of social security systems.

- The rising cost of benefits. For a variety of reasons, in particular the ageing population, there is an inexorable increase in the cost of benefits.

- Attitudes are slow to change and it is difficult to reduce or remove benefits in response to changes in circumstances. For example, 30 years ago here was an assumption that the elderly were by definition poor. That is no longer the case. The Jersey Opinions and Lifestyle Survey Report 2024 stated that the proportions of people who reported that they found it difficult to cope financially ranged from 82% for single parents to 47% for couples with children, 36% for working age people living alone and 24% for pensioners. However, pensioners still enjoy many benefits, such as free bus travel and drugs, merely because they are old.

The social security system in Jersey – context and overview

The point has been made that social security systems cannot be viewed in isolation but rather must be considered as part of a range of government policies with the objective of helping those who most need it. The social security system in Jersey must be seen as just one of five related strands –

- Economic growth, which reduces the demand for benefits particularly in respect of unemployment, and provides the funds necessary to pay benefits.

- The income tax system as the primary means of redistributing income from the better off to the less well off. Jersey's income system does this not through differential rates but rather through a very high threshold, that for a single person being £20,700 compared with the UK figure of £12,570 and Guernsey’s £14,600. The high threshold means that 23% of all personal income tax is paid by the 3% of taxpayers with the highest incomes. 400 taxpayers, 0.7% of the total, contribute 11%. Conversely, 21,500 taxpayers, 40% of the total, with the lowest incomes contribute 9%.

- A formal social security system funded by contributions from employees, employers and tax revenue, which primarily funds pensions but also illness, incapacity, unemployment, death, maternity and other benefits. Pensions are based on the period for which contributions are made not the amount of the contributions.

- An income support system funded entirely by tax revenue which provides direct financial support to those on the lowest incomes.

- A Long Term Care Fund, funded by a 1.5% additional tax on income, which meets long term care costs above a specified level.

The basic legislation is the Social Security (Jersey) Law 1974. This is supplemented by numerous orders covering contributions and benefits and also reciprocal arrangements with other countries.

Social security contributions and benefits

Details of the current benefits are set out on the Benefits and financial support page of the Government website.

The current contribution rates (excluding long term care contributions) are -

- Class 1 Contributions (Employed Individuals):

- Employee Contribution:only due if someone earns over the lower earnings limit of £553, but if that is exceeded then 6% of gross monthly earnings up to the upper limit of £5,800.

- Employer Contribution: as for employee contributions but at 5%, plus an additional 2.5% on monthly earnings above £5,800, up to an upper earnings limit (£26,442 - £317,304 a year).

- Class 2 Contributions (Self-Employed and Non-Employed):

- Individuals who are self-employed or not working for an employer are liable to pay Class 2 contributions if they are over school leaving age and have been resident in Jersey for at least six continuous months, at a rate of 5% on annual income up to the standard earnings limit (£69,600), plus an additional 2.5% on earnings between the standard earnings limit and the upper earnings limit (£317,304).

It will be noted that employer contributions exceed employee contributions both because they are at a higher rate, 6.5% as against 6.0%, but also because of the additional 2.5% on incomes above £69,600 a year. Self-employed people are in exactly the same position as employed people and employers combined.

Jersey’s contribution rates are significantly below those of the UK where the basic rate for employees is 8% with an additional 2% for those on higher incomes while employers pay 15%. Guernsey’s rates are similar to those of Jersey, 7.4% for employees and 7.0% for employers.

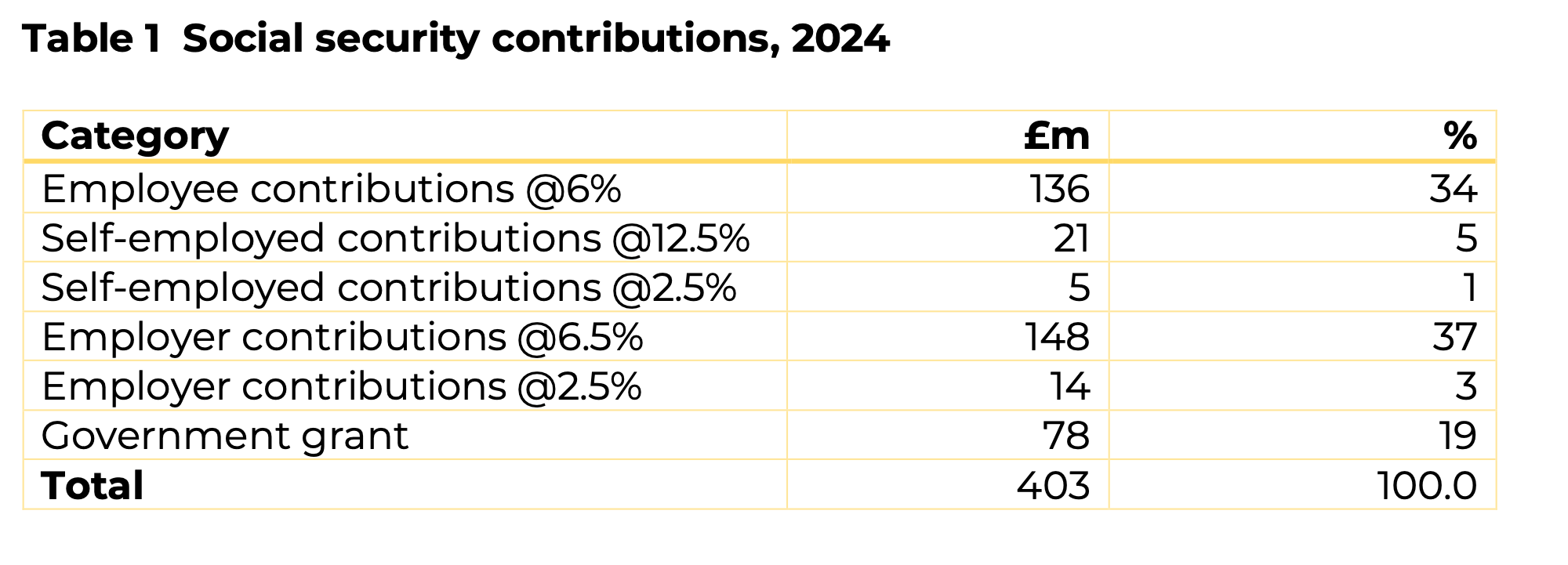

Table 1 shows the estimated breakdown of contributions between the various categories in 2024.

Source: Policy Centre estimates based on figures in the Government Plan 2024-2027 and the States of Jersey Group Annual Report and Accounts, 2024.

It will be seen the 40% of contributions were made by employers and 34% by employees. The self-employed contributed 6%, of which 3.6% can be attributed to their capacity as employers and 2.4% to their capacity as employees.

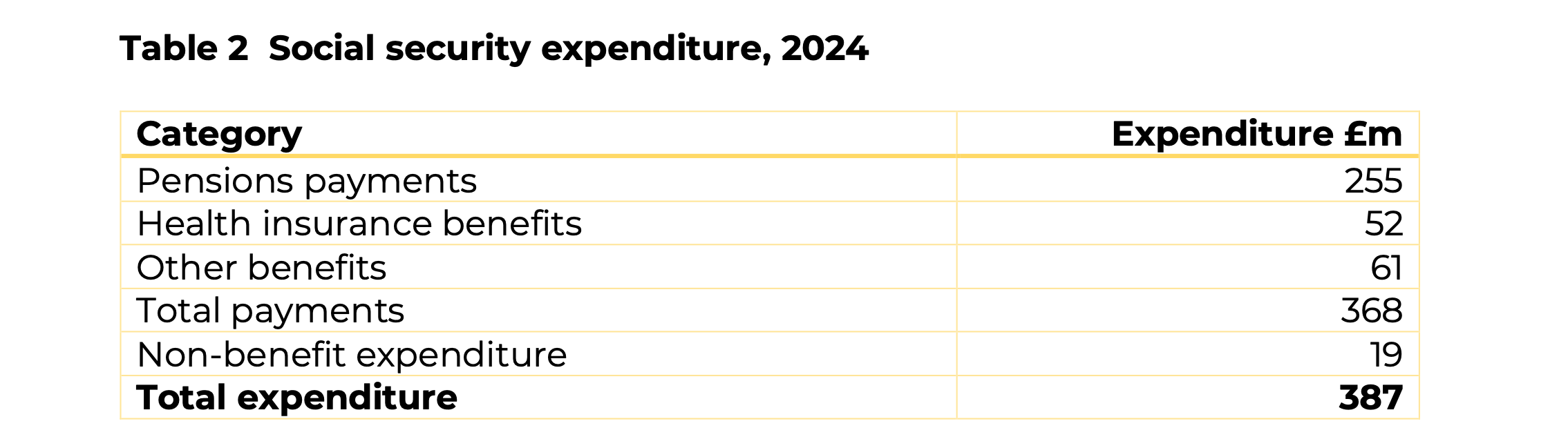

Table 2 shows how the revenue raised in 2004 was spent.

Source: Policy Centre estimates based on figures in the Government Plan 2024-2027 and the States of Jersey Group Annual Report and Accounts, 2024.

Pensions

Pensions are paid to those over 67 who have paid social security contributions for at least four and a half years. To get a pension at the full rate contributions must have been paid for between 45 and 47 years, depending on age. The current full rate old-age pension is £286.51 a week (£14,899 a year). For a married couple receiving a pension based on the contributions of the husband, the maximum rate is £475.65 a week (£24,733 a year). The pension is not related to the amount of contributions. Someone who has paid the maximum contributions receives the same pension as those who have paid much less.

Pensions are increased every October. The Government website states that the Jersey Average Earnings Index and the retail prices index (inflation) are used to work out the value of the pension: “This ensures pensions generally increase in line with the growth in earnings and takes into account increases in the cost of living.”

The basic state pension of £14,899 a year is higher than the comparable UK figure of £11,973 and similar to Guernsey’s £14,576.

At the end of 2024, 33,427 people received a Jersey pension –

14,729 men, 529 aged 90 and over

18,698 women, 1,202 aged 90 and over

Of the total –

19,303 lived in Jersey

7,725 lived in the UK or other Channel Islands

4,911 lived in other European countries

1,348 lived in other countries.

Those living in Jersey were far more likely to be receiving a full pension than those living elsewhere, many of whom had worked in Jersey for only part of their working lives.

The Social Security (Reserve) Fund largely exists to meet future pension liabilities. So, for example, if no further contributions were made, the fund would be able to pay pensions to those who have made contributions in the past. The Fund has been built up since the 1990s and stood at £2,452 million at end-2024, an increase from £2,179 million at the end of 2023 as a result of investment gains.

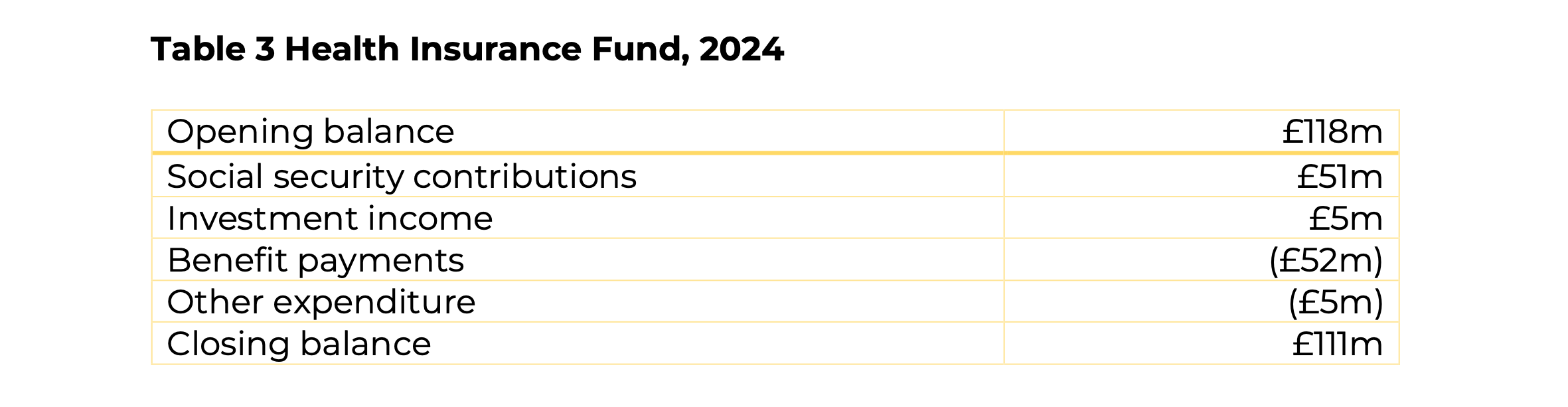

The Health Insurance Fund

The Health Insurance Fund is a discrete subset of the social security system, funded by general social security contributions rather than a specific levy. Of the total employee contribution of 6%, 0.8% is allocated to the Health Insurance Fund, and of the employer contribution up to the standard earnings limit 1.2% is allocated to the Fund. The relevant law is the Health Insurance (Jersey) Law 1967. The fund provides financial assistance to Jersey residents who need access to general practitioner (GP) services, in particular by partially offsetting the doctor's consultation charge and meeting in most cases the full cost of drugs prescribed by the GP.

Table 3 shows figures for the state of the fund in 2024.

Source: Budget (Government Plan) 2024-2027.

In 2024 the fund paid -

- For 2.2 million prescriptions at a cost of £19 million plus dispensing fees of £9 million.

- For 8,848 beneficiaries of the Health Access Scheme at a cost of £1.9 million.

- For 83,588 people to meet payments to GPs and for pathology tests at a cost of £19 million.

On 18 February 2026 the Jersey Audit Office published a report Health Insurance Fund by the Comptroller and Auditor General. A summary of the summary of the report is set out below -

The governance arrangements for the HIF involve a number of departments and include a range of strategic, operational and working groups as well as informal groups. The relationships and interdependencies between these groups are not formally documented.

No clear plan of action has been developed for the HIF since the 2021 actuarial review despite the clear indication from the actuary that the fund is not sustainable. Instead a number of additional benefits and contracts have been funded through the HIF since 2021 causing additional pressure on the sustainability of the HIF. The current funding and expenditure model for the HIF is not sustainable without intervention. There is commitment to an overall review of the healthcare delivery model including primary care which will include consideration of the HIF.

There has been a substantial increase in funding initiatives from the HIF to support improvements in GP practices and community pharmacies in the last few years. In the period from 2022 to 2026, the additional investment available in support for general practice is estimated at £12.3 million. From 2023 to 2026, the additional investment available for pharmacies is estimated at £12.4 million.

In the same period, significant additional funding has been provided from the HIF to improve access to general practice by increasing benefits and subsidies available to all eligible patients. The annual cost of this is estimated at over £16 million.

Investment in new schemes and initiatives has resulted in ongoing improvements to the breadth of primary care services, as well as reducing the cost barrier to accessing primary care services.

I have considered the key changes made in HIF expenditure since 2023 and whether they have been supported by robust business cases. Some of these changes related to States Assembly decisions, including approved Government Plan amendments. I did not observe consistency in the rigour with which business cases have been documented and did not observe good practice being adopted in some business cases supporting decisions involving significant investment.

Overall, my analysis suggests that new initiatives have been introduced without a full and consistent assessment of the long-term impact on the HIF and with insufficient consideration of resource and system implications. In addition, some initiatives lack the metrics to enable assessment of value for money following implementation.

Other social security benefits

There are a number of other benefits funded by social security contributions. The main ones are -

- Long-Term Incapacity Allowance for illness or disability. In 2024, 4,477 people received the allowance, payments totalling £28.7 million.

- Short-Term Incapacity Allowance for illness or disability. In 2024, 16,364 people received the allowance, payments totalling £19.5 million.

- Parental Allowance and Parental Grant for new parents. In 2024, 2,656 people benefitted at a cost of £5.0 million.

- Survivor's Benefit/Pension, provided after the death of a partner.

- Death Grant:a one-off payment following a death.

- Home Carer's Allowance:for those caring for someone with a long-term illness or disability.

- Insolvency Benefit.

The total cost of these benefits is small compared with the cost of pensions.

The long-term care fund

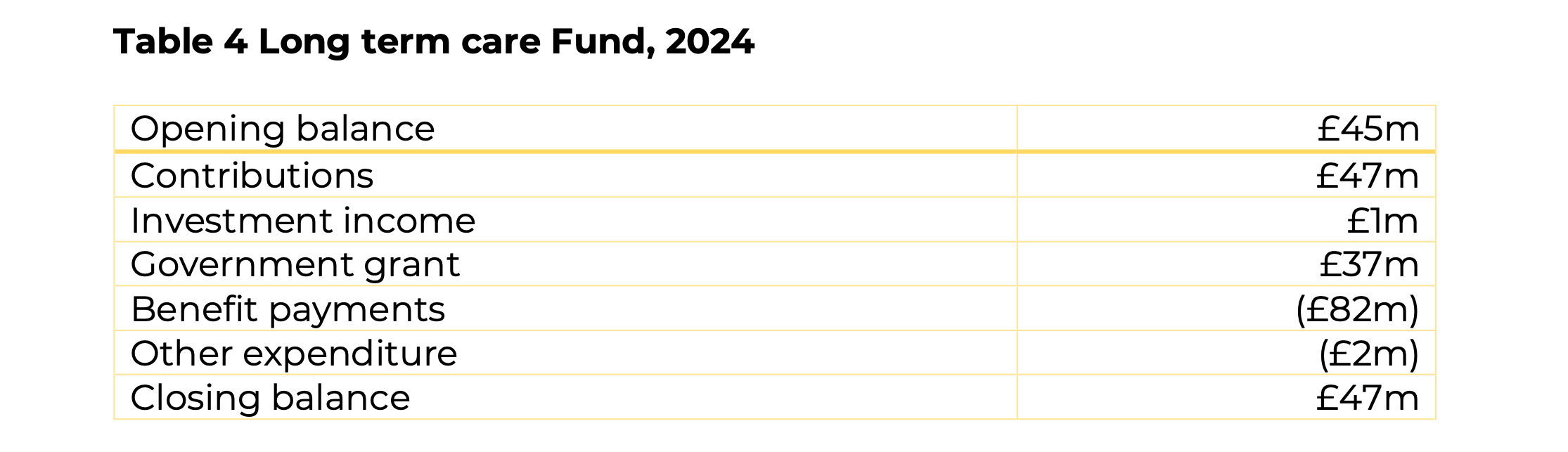

Unlike the Health Insurance Fund, which is funded by social security contributions, the Long Term Care Fund is funded through a specific tax. Jersey residents pay a Long-Term Care contribution at a rate of 1.5% on their gross earnings, up to the upper earnings limit for social security (£317,304 for 2025). The relevant law is the Long term care (Jersey) Law 2012.

The Fund provides financial support to Jersey residents who need long-term care for the rest of their lives, either at home or in a care home. It is means tested, taking account of income and assets. There is no similar scheme in the UK.

At the end of 2023, 1,463 people were receiving assistance from the Fund.

Table 4 shows figures for the state of the fund in 2024.

Source: States of Jersey Group Annual Report and Accounts, 2024.

It will be seen that contributions were equal to just 57% of benefits, necessitating a substantial government grant to meet the shortfall. This has been the position for some years.

Income support

Income Support is a single, means-tested benefit that gives people with income and assets below stipulated thresholds ,and who have been resident for at least five years, support to meet the costs of housing, living, health needs and childcare. It also makes provision for the role of carers for sick or disabled people.

The Income Support system is designed so that people who get Income Support and who work will always get a financial benefit from working. It does this by ignoring some of the income from work. Income Support is not subject to income tax.

The cost of the Income Support scheme is met by tax revenue not social security contributions and eligibility for Income Support is not dependent on having paid social security contributions.

The scheme is governed by the Income Support (Jersey) Law 2007. It is described in detail in a 130 page paper Income Support Policy Guidelines.

In 2024 expenditure on income support was £78 million, made up of -

Living costs £37.4 million

Accommodation costs £35.4 million

Other costs £6.5 million

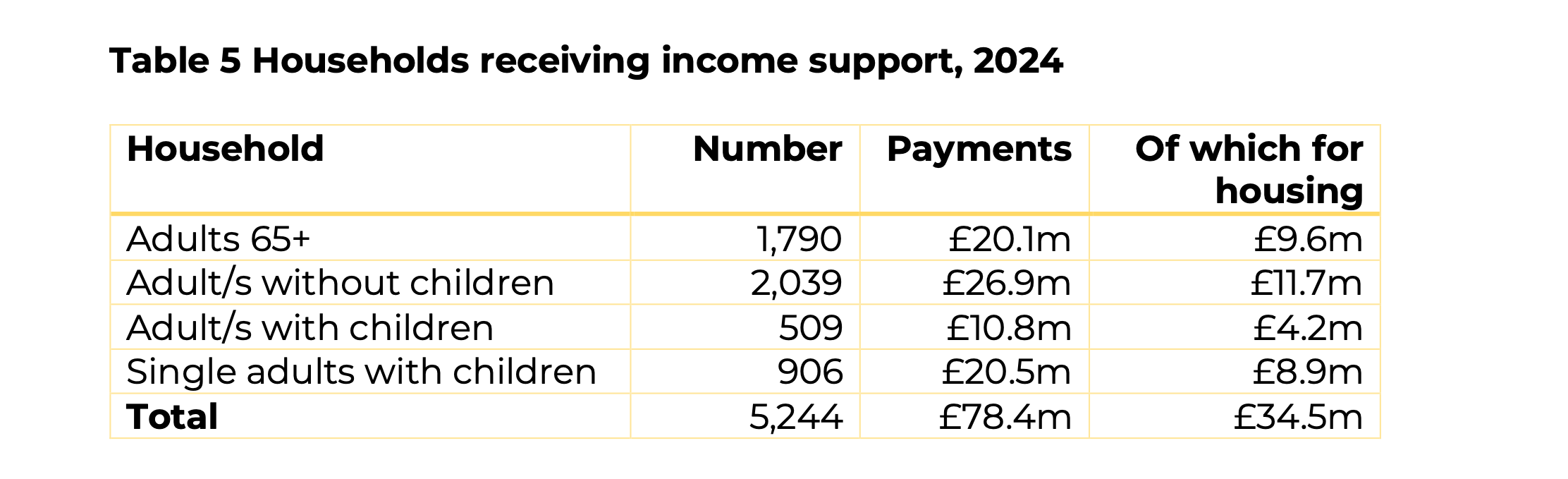

Table 5 shows a breakdown of expenditure between types of household.

Source: https://opendata.gov.je tables on income support claims and expenditure.

Of the accommodation costs total, Andium Homes (the Government-owned social housing provider) accounted for £21.5 million, other housing trusts £4.9 million and private landlords £7.8 million. Payments to owner-occupiers were negligible.

Community Cost Bonus

The Community Costs Bonus is an annual payment to help households with cost of living pressures. It is available to households of which one resident has lived in Jersey for at least five years, the household had a combined tax liability of less than £2,735 for 2024 and no member of the household is claiming income support. The Community Cost Bonus for 2025 is £516.50. People eligible for this benefit are also eligible for a Cold Weather Bonus when temperatures fall below a certain level.

Long term trends and issues

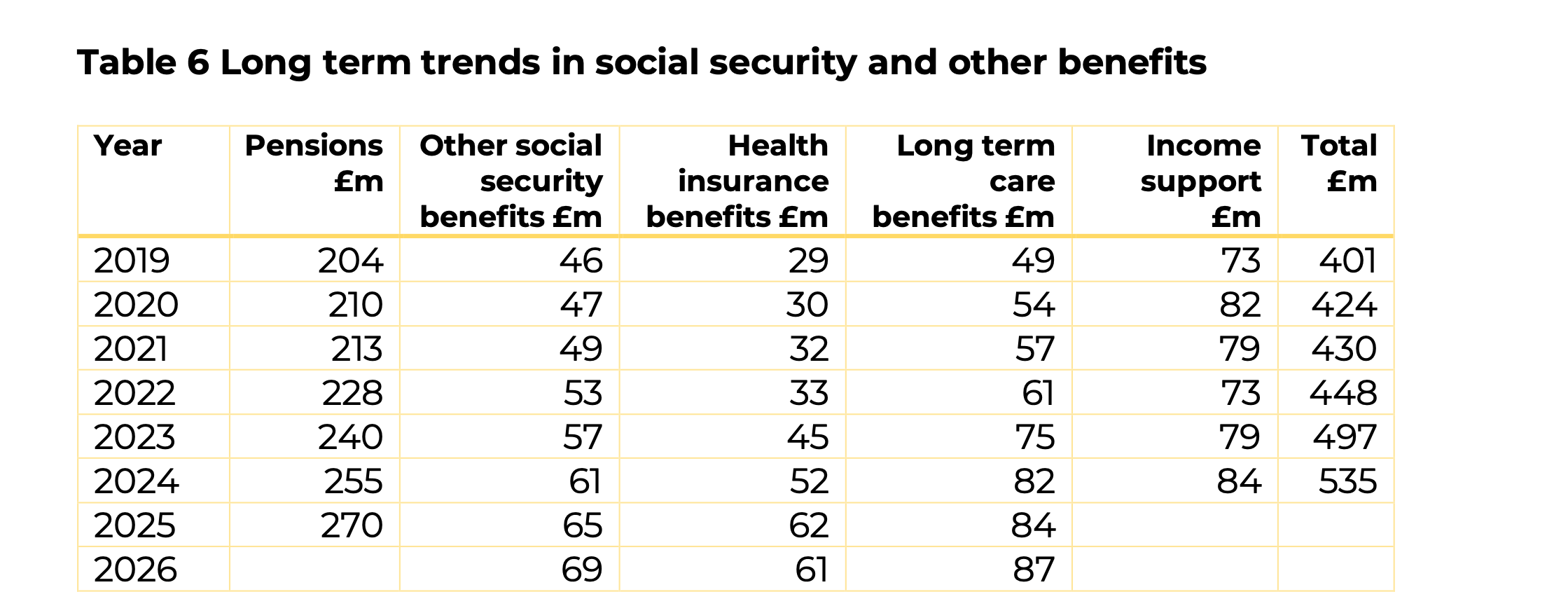

Table 6 shows trends in social security benefits and income support since 2019.

Sources: States of Jersey Group Annual Reports and Accounts for 2019-2024; 2025 and 2026 estimates are from Budget 2025-2028.

Notes:

- In 2019 Covid-related benefits of £112 million were also paid.

- The 2025 Budget gives a total for all social security benefits of £335; the split between pensions and other benefits is a Policy Centre estimate.

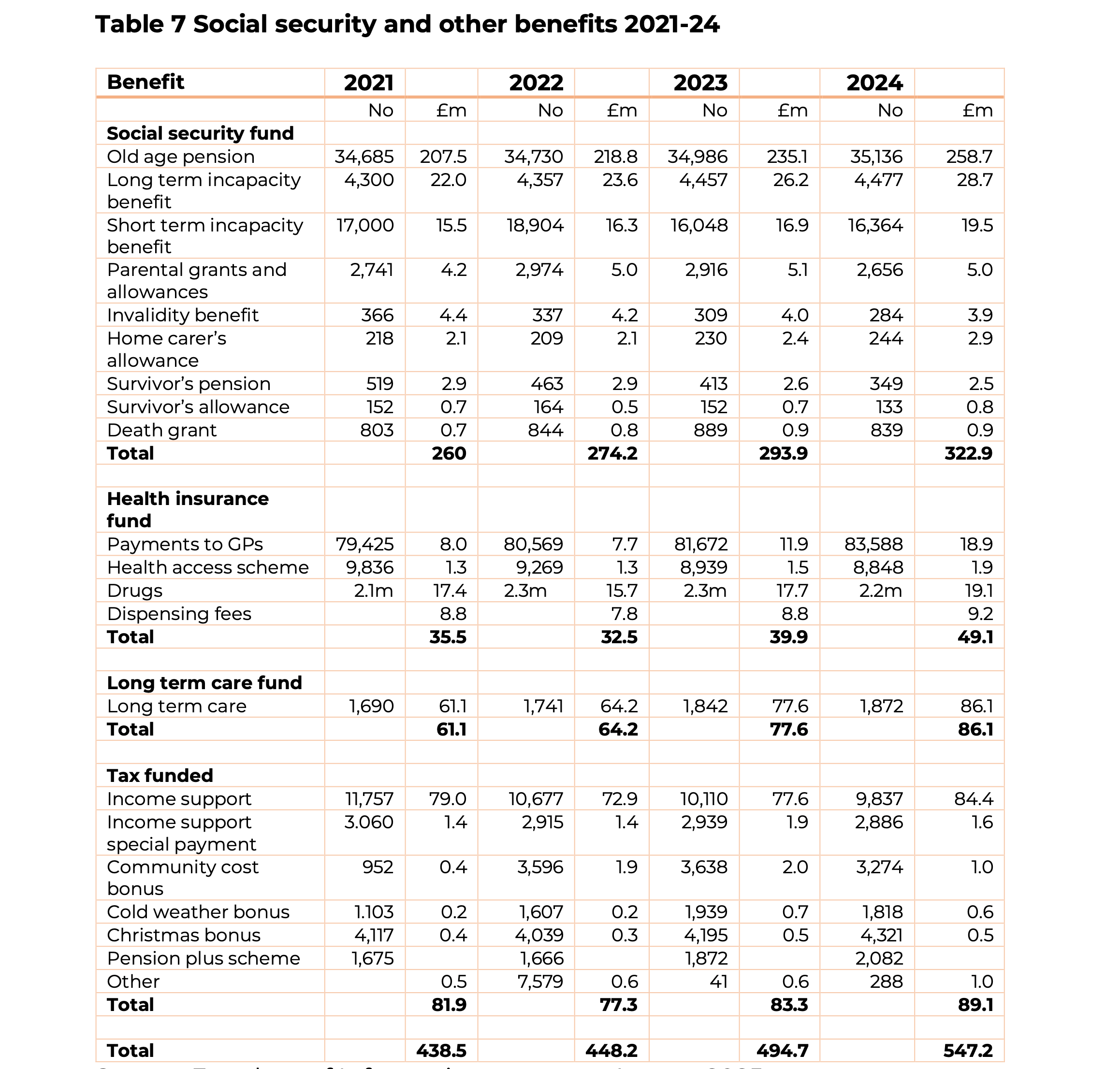

Table 7 shows detailed statistics for all benefits from 2021 to 2024.

Source: Freedom of Information response, August 2025.

In the five years between 2019 and 2024 benefits increased by 33%, not significantly greater than the increase in prices over this period of 29%. This is a significantly lower rate of increase than that in the United Kingdom. Jersey has managed to avoid a social security system that has led to a huge increase in the cost of long-term incapacity.

A review by the British Government Actuary of the combined state of the Social Security Fund and the Social Security Reserve Fund at the end of 2021 concluded that the combined fund “remains in good health and is expected to be able to pay benefits out for several decades under a range of scenarios considered”. A report by the Government Actuary on the Health Insurance Fund as at end-2021 said that “the Fund is projected to decline over the 20 year projection period, in current earnings terms, and be exhausted by around 2037-2041.”

Jersey faces similar long term issues in respect of social security to other jurisdictions although the problems are not as acute as those in many other countries.

A key issue is the ageing population which will put a significant strain on the ability to fund pension payments, although as Jersey has assiduously built up a fund to meet future pensions it is well placed compared with many other countries, particularly those that fund benefits from current contributions.

On 9 December 2023 Statistics Jersey published Population Projections 2023-2080. The report analyses the future size and structure of Jersey’s resident population under different scenarios of births, deaths and migration pattern. With net nil migration, between 2022 and 2050 the number of people over 64 will increase from 19,600 (19% of the population) to 26,410 (27% of the population).

A second general problem is finding the right balance between an affordable system and a generous system, something on which the British government is currently facing great difficulty. Table 6 suggests that so far Jersey has handled this fairly well and has not shown the huge increase in incapacity benefits that the UK has experienced.